TOP STORY: The Multi-Provider Era Just Started (And Most CTOs Aren’t Ready)

OpenAI declared internal “Code Red” this week.

Not because of technology failure. Because of competition.

Google Gemini 3 and Anthropic Opus 4.5 are forcing OpenAI to fast-track their new reasoning model, Garlic. They’re delaying major projects to ship faster.

For enterprise CTOs, this changes everything.

Here’s what I’ve been thinking about:

When your primary AI provider hits panic mode, what happens to your roadmap?

The answer depends on whether you planned for multi-provider reality or assumed single-vendor stability.

The AI Giants Aren’t Betting on One Horse. They’re Hedging Across the Field.

OpenAI signed a $38B, seven-year compute deal with AWS, ending Microsoft exclusivity. Microsoft and Nvidia are pouring up to $15B into Anthropic in exchange for $30B Azure commitment.

The uncomfortable question:Is your enterprise doing the same?

Most aren’t. I’ve seen organizations lock into OpenAI APIs assuming long-term stability. That assumption just became expensive.

Because here’s what multi-provider competition means for you:

1. Faster innovation cycles(good for capabilities, bad for stability)

Models update faster. Your integration breaks more often. Your team spends more time on compatibility rather than building value.

2. Higher migration costs

When your preferred provider lags behind, switching isn’t simple. Prompt engineering doesn’t transfer cleanly between models. Fine-tuning starts from scratch. Your agents need retraining.

3. Vendor-specific lock-in risks

OpenAI’s function-calling syntax ≠ Anthropic’s tool use ≠ Google’s function declarations. You’re not just picking a model. You’re picking an ecosystem.

Anthropic grew to 300,000+ enterprise customers this year - seven times more large accounts. That’s not random. Regulated industries (finance, legal, healthcare) are choosing reliability over raw capability.

AWS CEO Matt Garman said this week:

“AI agents will have as much impact on your business as the internet or cloud computing."[source]

Bold statement. But he’s right about one thing:the architecture you build today determines whether you benefit from AI competition or get trapped by it.

What changed this week:

The multi-cloud playbook from 2015-2020 is back. But for AI models, not infrastructure.

You need:

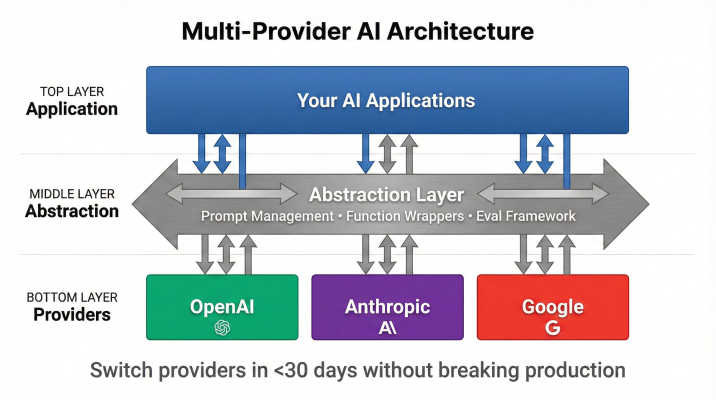

-Abstraction layersthat work across providers (so switching doesn’t break production)

-Benchmark-driven selection(not brand loyalty)

-Governance that survives vendor churn(policy independent of platform)

The organizations building this now will capture AI ROI. The ones waiting for “the winner to emerge” will pay premium migration costs in 2026.

Because here’s what “Code Red” really means: There is no stable single provider anymore. The AI market just entered permanent competition mode.

Your Board will ask: “Are we prepared for our AI provider to pivot strategy mid-deployment?”

Do you have an answer?

WEEKLY ROUNDUP: 5 AI Developments That Impact Enterprise

1. OpenAI Declares “Code Red” - Accelerates Project Garlic

OpenAI escalated to internal “Code Red” status this week after losing 6% of daily active users following Gemini 3’s launch. The company is fast-tracking a new reasoning model, “Garlic,” while freezing non-essential projects. CEO Sam Altman’s memo: “I wouldn’t trade positions with any other company” - signaling the pressure is real.

For enterprise:When your AI provider enters crisis mode, your roadmap is at risk. Multi-provider architecture isn’t optional anymore.

Source:CNBC: OpenAI Code Red - Google, Anthropic competition

2. The Competitive Squeeze: Gemini 3 and Opus 4.5 Reshape the Market

Google’s Gemini 3 captured 650M monthly users and outperformed GPT-5 on reasoning benchmarks. Anthropic’s Claude Opus 4.5 became the enterprise standard for coding and complex reasoning. This one-two punch triggered OpenAI’s crisis - proving that frontier model leadership can shift in weeks, not years.

Strategic lesson:Single-vendor dependency = business continuity risk when model performance leaps happen quarterly.

Source:CNBC: Anthropic shows strong momentum with enterprises

3. OpenAI Security Breach Exposes Developer Data via Mixpanel

OpenAI confirmed breach at partner Mixpanel exposed names and emails of developer platform users. Critical data secure, but vendor risk spotlight intensifies.

Bottom line:Audit your AI vendors’ third-party integrations. The attack surface isn’t just the model - it’s the ecosystem.

Source:X (pmainardi): OpenAI security breach report

4. Anthropic Momentum: 300K+ Enterprise Customers, 7x Growth

Anthropic reports sevenfold increase in large enterprise accounts, focusing on API stability for regulated industries. Strong signal: Enterprises choosing reliability over cutting-edge in finance/legal/healthcare.

Strategic insight:Multi-model strategy = hedge against provider instability AND capability gaps.

Source:CNBC: Anthropic shows strong momentum with enterprises

5. DeepSeek-Math-V2 Outperforms GPT-5 on Mathematical Benchmarks

Chinese model DeepSeek achieves IMO gold medal level and 61.9% on ProofBench, beating GPT-5 via generator-verifier system.

For enterprise:Specialized models for finance/engineering calculations may outperform general-purpose LLMs. Don’t default to brand names for quantitative tasks.

Source:X (pmainardi): DeepSeek-Math-V2 release

This Week’s Action Items:

Audit vendor lock-in risk- Can you switch AI providers in <30 days without breaking production? If no, that’s your Q1 priority.

Build abstraction layers- Prompt management, function-calling wrappers, eval frameworks that work across OpenAI/Anthropic/Google.

Plan governance independent of vendor- Your AI policy should survive provider pivots. Most don’t.

The multi-provider AI era started this week. The organizations that adapt to permanent competition will win. The ones waiting for stability will pay migration premiums.

What’s your multi-provider strategy?